CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Rachel Adams-Heard and Kiel Porter

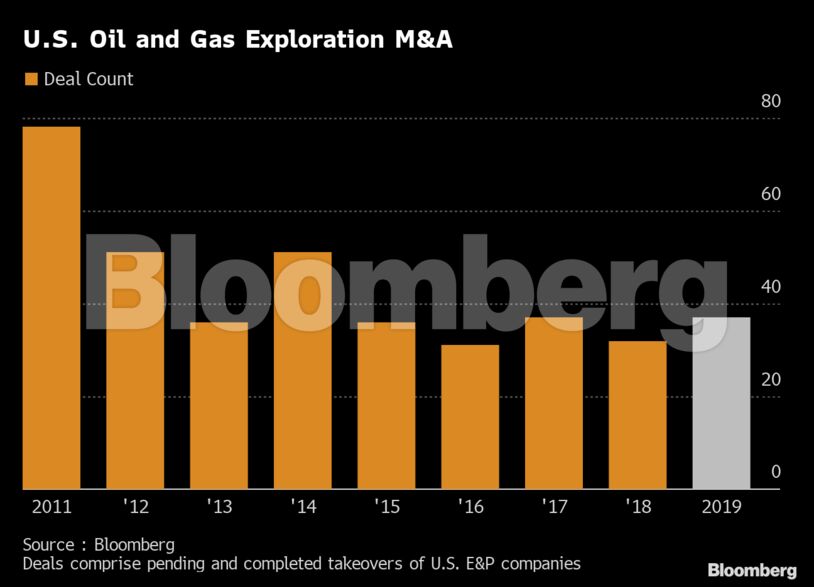

There has been $76.2 billion of mergers and acquisitions targeting U.S. exploration and production companies in 2019, according to data compiled by Bloomberg. That’s the highest going back at least 21 years, but it’s skewed by the takeover of Anadarko for $53 billion including debt. While the deal count rose to 37 from 32 last year, it remained below the number of transactions seen at the start of the decade, when oil and and gas prices were higher.

“Generally it’s been a slow year for dealmaking,” said Brittany Sakowitz, a partner at Vinson & Elkins. “I see 2020 being a lot of the same.”

Only one major energy deal this year came with effectively no premium: PDC Energy Inc.’s acquisition of SRC Energy Inc. It was also perhaps the only transaction between two public oil producers to be widely applauded by analysts and investors. Unusually for an all-stock takeover, the shares of the acquirer, PDC, surged on the day the deal was announced.

When asked by one SRC shareholder why he didn’t get a premium for his stock, the company’s Chief Executive Officer Lynn Peterson replied that he had created a stronger, larger business with a lower cost of capital, according to Citigroup’s Trauber. An SRC spokesman confirmed that’s how Peterson has defended the merger.

“That’s the mantra investors have and want to see,” Trauber said.

What Bloomberg Intelligence Says:

“It would be difficult for management teams to agree on a low- to no-premium deal, especially considering they would tend to view it relative to where their stock prices were just one to two years ago”

— Vincent Piazza, senior analyst

What investors don’t want are expensive deals. Occidental outbid Chevron Corp. and secured a $10 billion commitment from Warren Buffett to buy Anadarko. But its stock is now headed for the worst annual performance in two decades. Billionaire activist investor Carl Icahn has said Occidental paid too much, and he’s pushing ahead with efforts to replace the company’s entire board, people familiar with the matter said last month.

The bidding for Anadarko initially sparked optimism that widespread consolidation may finally come to the crowded Permian Basin. But those hopes were dashed after just a few smaller oil producers followed suit, including Callon Petroleum Co., which acquired rival Permian operator Carrizo Oil & Gas Inc. Callon’s shares tumbled 16% on the day the deal was announced and extended their decline after public opposition from investor Paulson & Co. Callon was eventually forced to cut the takeover premium to get the deal done.

“The buyside does want consolidation, but they want it at very low premiums, and they want it for significant synergies,” said Tim Perry, co-head of Credit Suisse Group AG’s oil and gas investment banking group. “Those are the kinds of deals they will support.”

Still, the lack of a premium may act as a disincentive for some energy executives, as they would stand to receive less for their equity and stock options in a takeover than they otherwise might have done, at least in the short term.

“If you’re the CEO and somebody comes and says, ‘I want to acquire you,’ you’re going to have to pay a pretty big premium in order for me to lose my job,” said Noah Barrett a Denver-based energy analyst at Janus Henderson Group Plc, which manages $360 billion. “Self-preservation is a huge behavioral factor in the decision-making process for these guys.”

Share This: