CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Liam Denning

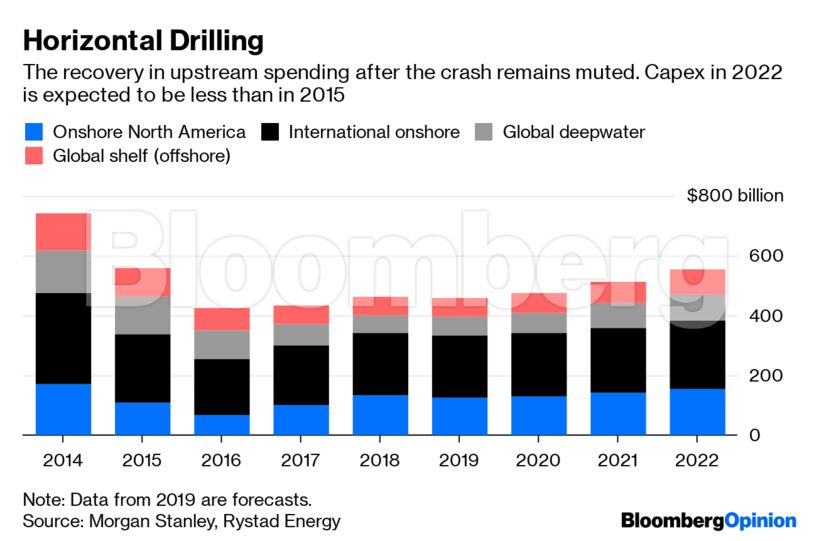

The oily water in which the services companies swim is the money that exploration and production firms spend – and it has dried up. Analysts at Morgan Stanley have just reduced their forecasts for upstream capital expenditure. In the title of the report, “Global Upstream Capex: Growth Still in the Cards,” that “Still” does most of the work.

At around $65 a barrel, oil remains well below those triple-digit salad days of early 2014. Still, it’s about double where it was in early 2016, and yet there’s precious little sign of that in E&P capex budgets. Something structural has happened.

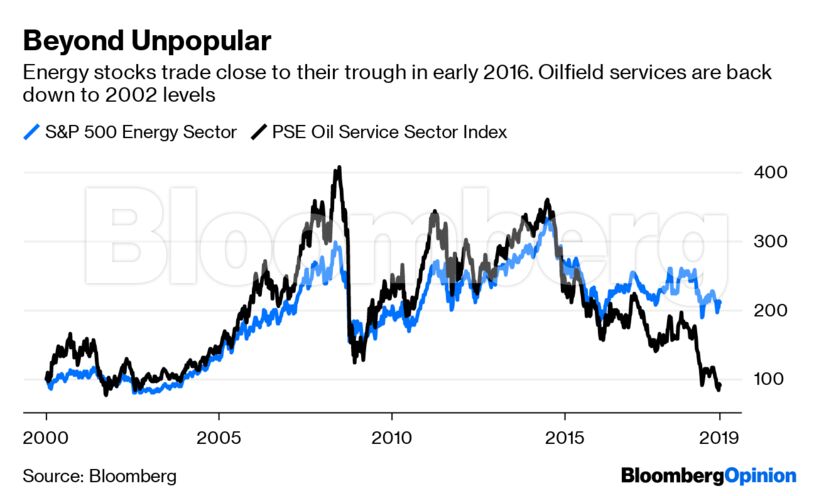

E&P stocks are unpopular because a decade of high spending did wonders for oil and gas output, “energy dominance” and C-suite pay, but little for investors. So the latter have gone on strike, demanding evidence of a change of heart on the part of management teams, chiefly in the form of tighter spending and more generous payouts to shareholders. You can see the problem for oilfield services, which profited nicely from the E&P sector’s pre-2014 largesse.

At the same time, E&P companies still like to grow, so the pressure to do more with less remains high (especially as activists have begun beating the drum on this). Last year’s surge in U.S. oil and gas production was the biggest achieved by any country ever, according to BP Plc, even as upstream capex there was still 22% below the level of 2014.

E&P companies depend on their services providers to help achieve the productivity gains that have fueled the shale “miracle.” Yet the rewards for this – such as they are – have flowed overwhelmingly to the client, not the contractor. A decade ago, the oilfield services sector earned a return on capital employed that was more than 13 percentage points higher than the E&P sector, according to analysts at Evercore ISI. By 2018, the sectors had switched places, with services earning 7 percentage points less than their clients. That is some transfer of value.

The oilfield services industry shares some pathologies with the E&P business. Contractors invested too heavily in the boom, creating excess capacity and bloated cost structures. When the crash hit, they prioritized market share, the standard response in expectation of an eventual rebound – and the rebound hasn’t taken off. General Electric Co.’s ill-timed foray into the business via Baker Hughes and Weatherford International Ltd.’s meandering shuffle into chapter 11 have provided unwelcome narratives for all this. Today, despite deals such as the recently announced merger between Keane Group Inc. and C&J Energy Services Inc., the sector remains fragmented, particularly in those areas such as pressure pumping that service the U.S. shale industry.

Shale is a blessing and a curse. On one hand, it has accounted for all of the growth in global upstream capex since the trough in 2016 and is set to contribute 29% of the forecast growth from here through 2022. On the other, it is a fragmented corner of the business that is highly sensitive to oil prices and has flattened the cost curve across the global industry. Besides trade-war concerns, expectations of frackers taking advantage of any geopolitical spike in oil prices to boost production have helped to keep a lid on that spike, despite numerous provocations.

The upshot is a very narrow band in oil prices between celebration and belt-tightening. Morgan Stanley estimates $50 oil in 2020, as opposed to $60, would cut expected cash flow from operations in the global upstream business by a fifth, translating to a 13% drop in capex – which would take it below 2016 levels.

Faced with such sensitivities, investors aren’t willing to pay a premium. Bellwethers Halliburton Co. and Schlumberger Ltd. trade at Ebitda multiples similar to where they were in 2015, when spending was headed down, rather than being priced for growth. Spending should grind higher from here; even so, the sector faces a deep-rooted challenge. For E&P companies to win favor with investors again, they must adhere to a regimen that won’t help their contractors win any popularity contests.

Share This: