CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Rising Oil Prices Will Test Frackers

We see oversupply, oversupply and oversupply of both oil and gas …

That particular respondent from the oilfield services sector, featured in Wednesday’s release, sure seems concerned about something. As well they might. Oilfield services stocks are even less popular than those pariahs known as exploration and production stocks. The reason, as I laid out here, is that the route back to redemption for E&P companies involves diverting more cash flow toward shareholders and less toward the sort of spending that boosts the top line for oilfield services contractors.

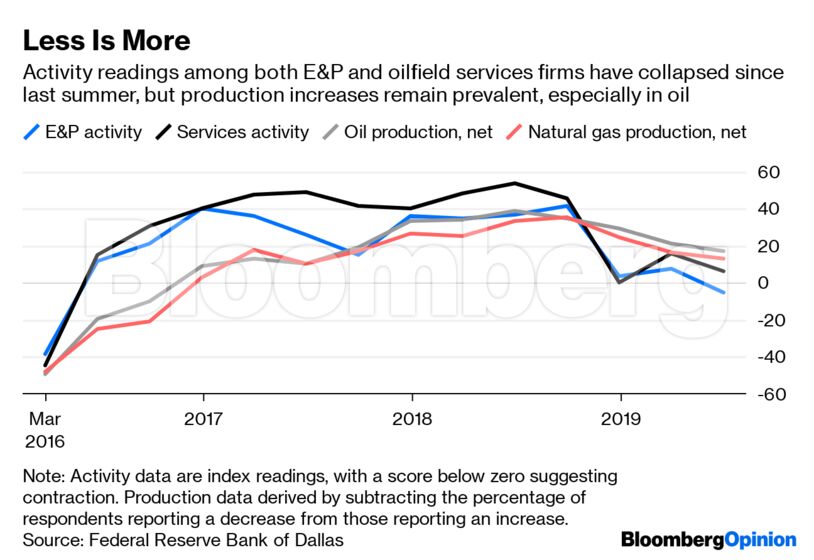

The sector’s problems can be summed up in this chart. It shows index readings for business activity among E&P and services firms, as collated by the Dallas Fed. It also shows readings for the change in oil and gas production. These numbers are derived by subtracting the percentage of companies reporting a decrease in output from the percentage reporting an increase (I ignore the proportion reporting no change).

Back in early 2016, everyone knew where they stood: in a hole, with oil having just dipped below $30 a barrel. But activity and production bounced back relatively quickly. Most pertinent to the current situation is that uptick in activity and the prevalence of production growth, especially for oil, last summer. That was when expectations of imminent Iranian sanctions from Washington sparked a big rally in oil prices – and led E&P companies to quickly abandon the spending discipline they had touted in early 2018. The subsequent head-fake on Iran in the fall, combined with surging U.S. oil supply running into an unusually weak fourth quarter for demand, trashed prices, stocks – and the last sliver of credibility the sector had with investors.

As concerns about oil demand have blunted the impact of this year’s escalation in U.S.-Iranian tensions, so E&P firms have recommitted to discipline. That looks real enough, judging by the index readings on activity. Some respondents also mentioned the impact of disinterested investors and distrusting lenders in curbing drilling.

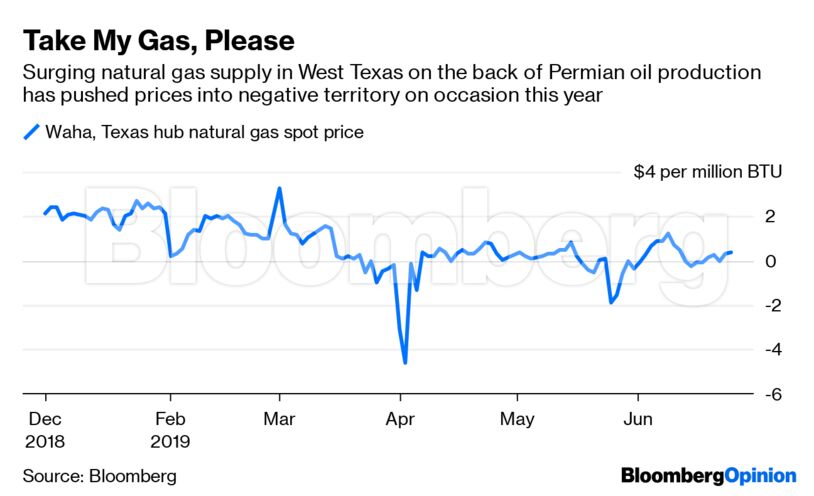

But juggernauts this big don’t brake on a dime. While the proportion of E&P firms telling the Dallas Fed that output fell has risen from about 18% in the fourth quarter of 2018 to about 26% in the current quarter, more than 70% report flat or increasing production, and weighted toward the latter. Even in natural gas, a market so awash that prices in West Texas have turned negative on some days this year, almost 40% of respondents reported an increase in production.

The cure for low prices is usually low prices, but the productivity gains of recent years in shalelandia – funded in part by contractors’ pain and investors’ prior indulgence – have kept moving that bar lower. The latest washout in stock valuations may provide the impetus needed for discipline to take hold, which could tempt investors back to the E&P sector (services, not so much).

The test for that may already be upon us. At the moment the dour Dallas Fed survey results went up Wednesday morning, the Energy Information Administration was reporting a big drop in oil inventories last week, pushing up prices. Naturally, the most highly levered, volatile stocks such as California Resources Corp. and Denbury Resources Inc. leaped.

A combination of a trade truce between the U.S. and China at this weekend’s G-20 festivities and more flare-ups in the Persian Gulf could provide a further tailwind for prices heading into the traditionally strong summer season for oil demand. Respondents’ comments suggest little faith in peace breaking out on trade; and one rather delicately indicated a different kind of war might be more relevant:

A reversal in the current supply/demand relationship will likely depend on the occurrence of an event or events that are less than desirable.

For investors, though, it’s less about what oil prices do and more about what E&P management teams do with them. If a summer spike reawakens the impulse to drill, we’ll get cheerier Dallas Fed readings at odds with listless stocks.

Share This: